The price of lithium carbonate and cobalt have both risen to two-year highs as lithium-ion battery demand and logistical issues linked to COVID-19 formed a perfect storm for the materials industry.

According to Benchmark Minerals’ February 2021 issue of the Benchmark Cobalt Price report, the cobalt market could fall into deficit later this year, with the deficit rising through the 2020s.

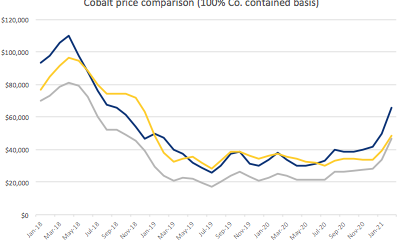

The report stated that year-to-date (YTD) prices for cobalt hydroxide rose 65.5% whilst cobalt sulphate and metal prices increased 56% and 42%, respectively.

The increase, the highest since Q3 2018, saw sulphate reach $65,780 per tonne (pt), metal $48,502pt and hydroxide rise to $46,750pt, in February.

Sulphate and metal recorded their greatest average monthly increase of more than $15,000 and $13,000, respectively, since January 2018.

Gregory Miller, analyst at Benchmark, said the cobalt price rise last month was attributable to both an acceleration in battery demand, tied to the surge in global EV sales since late 2020, and persistent logistics issues across the cobalt supply chain.

He told BEST: “Logistics delays are linked to sever ongoing issues attributable to the COVID-19 pandemic, including: a lack of domestic truck availability in China, a lack of available vessels to ship material and high shipping costs, limited capacity at Chinese ports to receive material, and residual delays across transportation networks in Africa.

“In particular, the availability of cobalt hydroxide has been affected by logistics delays across the cobalt supply chain, driving cobalt hydroxide payables to an equivalent of close to 100% of the prevailing metal price in late February. This price increase was acceptable to refiners due to the existence of a significant premium for cobalt sulphate over cobalt hydroxide/metal.

“Due to only a limited volume of cobalt hydroxide being available on a spot basis, Chinese refiners have moved to secure suitable metal units, fuelling tightness in cobalt metal availability and driving prices higher.”

The availability of cobalt hydroxide— the main cobalt feedstock for chemical conversion— has been affected by logistics delays across the supply chain, stated the report.

The report also noted how “extremely” limited volumes of cobalt from the Democratic Republic of the Congo had driven Chinese refiners to try and secure a suitable supply from Europe and global markets.

Lithium prices

The firm’s Benchmark Lithium Price Index report also noted that battery grade lithium carbonate prices increased by 68% in China during the first two months of the year.

Technical grade lithium carbonate reached $10,475/tonne, with battery grade lithium carbonate hitting $11,250/tonne, and lithium hydroxide closing out February at $8,825/tonne.

George Miller, at analysts at Benchmark, told BEST that pricing in China tended to be the bellwether of lithium market pricing.

He said: “Given the current pipeline for supply-side expansions and new lithium production, we expect a significant deficit in the lithium market balance to arise from 2021 onwards.

“Out until 2027, we see demand growth rates of approximately 20-25% each year, compared to limited supply-side expansions coming to market due to the low price environment and COVID-19 delays.

“This has created a critical challenge for upstream producers, whether incumbents or juniors looking to develop production capacity, to meet mounting downstream demand from the industry.

“In this case, there needs to be significant and sustained investment into lithium supply if market supply is to meet demand, not just from Chinese cell manufacturers, but from cell manufacturing worldwide.”

The price rise is believed to be on the back of high battery demand, particularly for lithium iron phosphate (LFP) cathode, and a slower-than-anticipated transition to high nickel chemistries.

Surging Chinese lithium carbonate prices, which now hold a premium over hydroxide prices for the first time since April 2018, helped push the Benchmark Lithium Price Index up by 14.4% in February, its second largest move on record after January 2021.

Demand for the material in China has remained high due to the “slow roll out of higher nickel cathode chemistries”, with the NCM (nickel, cobalt, manganese) cathode production still focused on NCM 523, according to the report.

The report noted: “Although the greatest price increases have been constrained to Chinese lithium carbonate, the global weighted average lithium hydroxide prices were up 8% year-to-date as prices increased on the back of improving EV demand sentiments.”

It added: “While large prices have so far been limited to China, pricing in the rest of the world has begun to move upwards towards Chinese levels with ex-Chinese carbonate prices up by an average of 17.1% in February.”