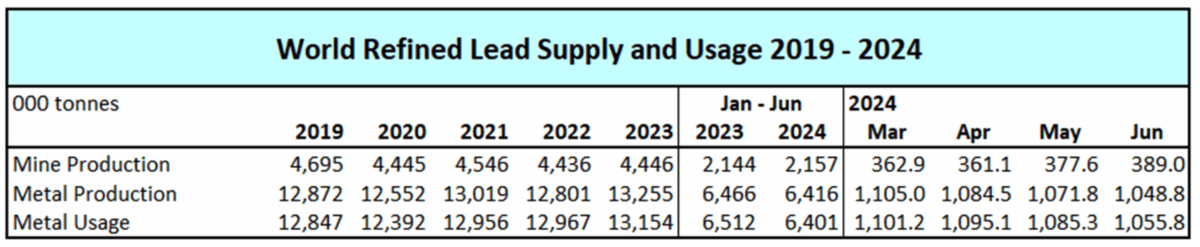

Global supply of refined lead metal continues to exceed demand. In the first six months of 2024, the surplus was 15,000 tonnes, according to provisional data released on 21 August by the International Lead and Zinc Study Group.

It said reported inventories rose by 93,000 tonnes.

World lead mine production rose 0.6% in the period. It was up in Australia, Kazakhstan, Peru and Sweden and down in Ireland, Portugal and the US.

ILZSG said production of lead metal fell 0.8% in the first six months – mainly a result of lower output in China and Canada.

Usage of refined lead metal fell 1.7% on a global basis. It was up in China, India, Japan and South Korea, but more than balanced by falls in Europe and the US, it said.

Chinese imports of lead contained in lead concentrates fell 10% in the first six months to 285,000 tonnes. Net exports of refined lead metal totalled 14,000 tonnes, a 57,000-tonne decline compared to the same period in 2023.

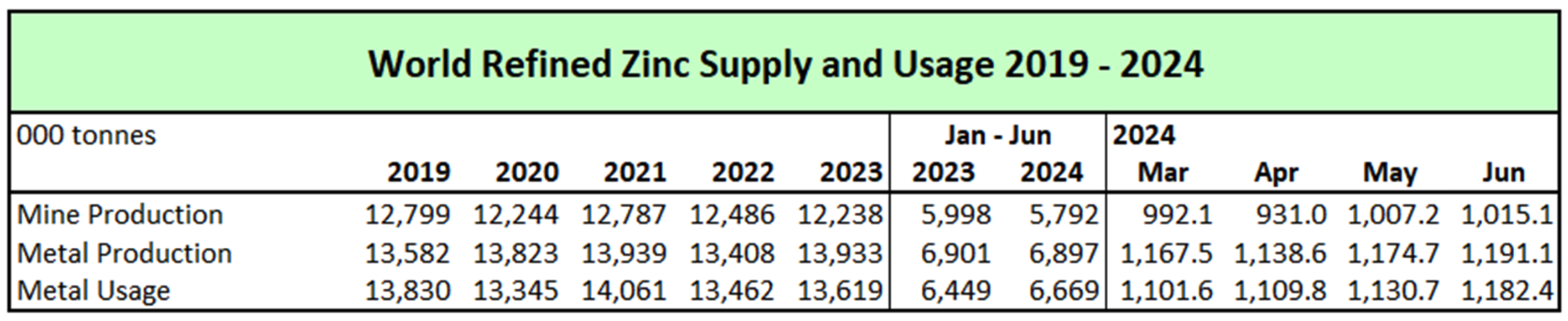

Zinc surplus

The global market for refined zinc metal showed a surplus of 228,000 tonnes in the first six months, according to provisional data. Reported inventories increased 172,000 tonnes in the period, the body said.

World zinc mine production fell 3.4%, it reported. This was influenced by dips in Canada, China, South Africa and Peru. Ireland and Portugal also saw lower production, caused by suspension of mining activity. Australia, Brazil, Mexico and Sweden saw higher output than the same period a year before.

Refined metal production was down a modest 0.1%.

The usage of refined zinc metal worldwide was up 3.4%, according to the data.

Chinese imports of zinc contained in zinc concentrates fell 24.6% to 819,000 tonnes, while net imports of refined zinc metal came to 216,000 tonnes. This represented a 122,000-ton increase from the first half of 2023.

All data sources: ILZSG